[Guest author today, Graham from MoneyStepper.com]

Getting out of debt isn’t easy. But, as many inspirations in the personal finance blogosphere have proven, it’s achievable. And when it is achieved, boy does it feel good!!

We see hundreds of figures every year on “The Average American” and that they are in a position of debt like never seen before. Well, today, we are going to get this average American, let’s call him Tay (“The Average Yank”), out of debt for good in under 3 years, with relative ease!

The Average American’s figures

To help Tay, we need to know a few things about him.

- Tay is 36.8 years old (based on the median American age)

- His household income is $51,017 (based on the median household income)

- Federal income tax is $2,590 and Social Security is $3,903 (based on the median income)

- Therefore, take home pay is $44,524

- He has credit card debt of $8,200 (average household debt 2011) , at 15% annual interest

- He has auto loans of $7,300 (average household debt 2011) , at 8% annual interest

- He has student loans of $6,500 (average household debt 2011), at 5% annual interest

- He has an outstanding mortgage of $104,000 (average household debt 2011), at 5% annual interest

- Household expenses per year are as follows:

- Transportation costs $8,800 ($733 pm)

- Food costs $6,200 ($517 pm)

- Insurance and pensions $5,400 ($450 pm)

- Medical expenses $2,850 ($238 pm)

- Clothing $1,900 ($158 pm)

- Entertainment $2,700 ($225 pm)

- Tobacco & alcohol $1,000 ($83 pm)

- Electricity & gas $1,600 ($133 pm)

Note: the sum of these expenses (plus a $6700 per year mortgage payment based on the outstanding mortgage above) only equals $37,120. This leaves this Tay with over $7k per annum unassigned expenses. I raise this point as everything I’m showing is easily achievable and, in reality, could be even easier if we factor in this $7k!!

Budget assault

So, what does Tay need to do?

Let’s firstly look at his budget and where to trim the fat. Then, we’ll attack the loans afterwards.

I’m going to assume (very kindly given that I’m sure this isn’t the case for Tay) that insurance and pensions includes only necessary insurance and that his pensions consist of a matched contribution to a 401k. Equally, I will assume that there are no savings to be made on medical expenses as these are all necessary.

What about the other areas?

Transportation costs

The Tay household is a two car family and they both drive an “average Sedan”. The average cost is 60.8 cents per mile and this leads to their transportation costs of $8,800. Many savings could be made through methods such as car pooling, taking public transport, cycling or a number of other ways. However, to minimize the impact on Tay, I am only going to suggest that he downgrades both his cars. If they both drive a “small Sedan”, the average cost per mile will fall to 46.4 cents per mile, and the Tay household will save $2,084 per year ($174 pm). Note that this also ignores the profit they will also make on selling their larger vehicles and downgrading to smaller second hand vehicles, and the potential impact this will have on their “auto loans”.

Food costs & Entertainment

To understand what could be spent in each of these categories, I’m going to take an average of spending on US blogs around the blogosphere:

| Site | Food expenditure | Entertainment |

| Budget Bloggess | $469 | $110 |

| Journey to Saving | $444 | $53 |

| Green Bay Consumer | $342 | n/a |

| Blonde on a Budget | $343 | $76 |

| Living Rich on the Cheap | $423 | n/a |

| Planting our pennies | $508 | $85 |

| The Frugal Farmer | $451 | $70 |

| AVERAGE | $425 | $79 |

By matching these figures, we could be saving $92 pm on food and $146 pm on entertainment.

Clothing

When in debt, there is no way that Tay needs to spend more than $100 pm on clothing. Let’s therefore assume a $58pm saving on clothing.

Tobacco & alcohol

Well, we all know we shouldn’t smoke – so we will have $0 on tobacco. However, I’ll let them have 2 bottle of wine and a 6 pack of beer each month, amounting to $30. Therefore, we also see a $53 saving in this category.

Budget assaulted!

Therefore, with very little impact on Tay’s life, we have saved his household $523 to place towards the reduction of debt.

Tackling the debt

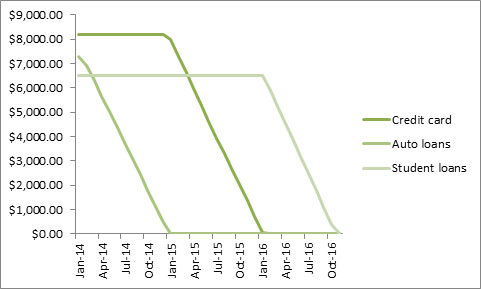

The first thing that Tay does is sign up to a 18 month 0% balance transfer credit card for his existing credit card debt. This costs 3% of the $8,200 ($246), but this shall be factored into the debt repayment schedule below.

After this, Tay will put his old minimal payments, combined with the $523 monthly saving to paying down his debt. Given that the credit card is now 0%, he can focus on highest interest auto loan, and then attack the credit card before the higher rates kick in, and finally remove his student loan:

So, for 2 years and 10 months, Tay and his family have to make some small adjustments to their lives. They don’t have to dumpster dive, they don’t have to starve and they don’t have to work every hour of every day to earn additional income. They just need to be sensible with their money and they will be debt free very soon.

Voilà – the problem of the “Average American” solved!!

——–

Graham blogs at MoneyStepper.com – a site that provides small steps, every day, which have a huge impact over the long-term. His regular posts cover topics concerning every aspect of money, investing and saving, which will help you increase your net wealth in the short, medium and long term.

Photo courtesy of hankinsphoto.com

Great article and breakdown of one very average American. I love that you showed just how possible it is to get out of debt – even though it will take some money management, discipline, and hard work to achieve it, it IS possible, and here’s the proof.

Thanks for the comment Kali – glad you enjoyed the article! And you are right, it really IS possible. Come on, we can do this Tay!!

Excellent, concise and entirely doable. The ultimate antidote to listening to people whine about being in debt forever when the solution is entirely in their hands.

Imagine what could be accomplished if Tay were willing to actually do anything uncomfortable (pick up a PT job, sell unused items around the house, cut the wine/beer, cut the clothing budget to only emergency replacements of footwear and winter clothing, plant a garden, drop to one vehicle and commit to more biking/or ride sharing, etc, etc.

Also, imagine what could be accomplished if even the basic changes outlined above were left in place after the debt was gone, and instead directed to retirement savings and/or getting rid of the mortgage asap. Early retirement anyone?

We did serious, emergency cutting of our spending following an unexpected layoff. The job was quickly replaced but the exercise of evaluating what could be cut and how much we’d been wasting was very enlightening. Being forced to temporarily cut down to just the essentials showed us that we didn’t actually miss most of what we’d cut out. That was many years ago and we never went back. The only nonessential we allowed back into the spending was an annual trip. Otherwise all the excess beyond the bare essentials goes to the mortgage and retirement savings. That layoff completely changed our lives for the better. We went from having no idea if or when we’d retire to knowing we can retire in our late 50s. If only we’d been forced to see the light decades sooner we’d already be retired.

Well said JMK – make these (and more) changes and just imagine where Tay could be!!

Love your story. Everyone who succeeds in paying down their debts has that “starting point” where something changed or something clicked. I’m glad you were able to keep it going for many years. Knowing that you will retire in your late 50s (or indeed at all) is a much better situation to be in than poor old Tay…

This is why people in debt need to budget. They need to see where their money is going to see where they can start making cuts. Well I think everyone should have a budget really.

Totally agree!! Someone really needs to make a website about budgets being sexy….!! 😉

It’s already been done…www.budgetsaresexy.com

The biggest thing is having a plan…and sticking to it.

We weren’t getting anywhere until we established a plan. Now, we follow a budget and have financial goals that are structured for success rather than the overwhelming feeling of financial chaos or of being deprived.

The debt snowball is always the way to go as well.

The Warrior

NetWorthWarrior.com

Great summary Warrior and thanks for the comment.

Step 1) Make a good, suitable plan

Step 2) Stick to it

It really just all comes down to this!

That looks like a good plan, now to tackle the American (Government) Debt!

Kevin – please feel free to forward to Mr. Obama!! 🙂

Sadly, I think a combination of not tracking expenses/budgeting comes down to being stubborn and in denial, and sometimes, lazy. My parents absolutely refused to cut their smoking habit, which cost them a lot, both financially and health-wise. It drove me nuts. I have to say they didn’t spend on extra items like clothes, and rarely went out to eat (I’m talking MAYBE twice-three times a year to a sit-down restaurant). The trouble is trying to find a balance where you’re happy with the progress you’re making toward debt repayment and making sure you don’t burn out during the journey.

Agreed E.M.

Unfortunately, when it comes to money and budgeting, Tay is pretty lazy! I think this is the biggest problem – the ease of paying for things on credit just seems to take less effort than keeping a well controlled budget.

This is why I’m so big about writing down expenses. You don’t realize how much you can cut out until it’s all laid out there in front of you with the numbers.

Completely agree Stephanie. You might think you are living on a shoestring, but without writing it all down, you’ll never know exactly where you are overspending!

It’s very interesting to see a plan laid out like this one. It shows how possible it really is to overcome debt!

Thanks for the comment Terry – glad you enjoyed the article. When we look at it like this, the amount of household American debt maybe isn’t as bad as the media makes out. The attitudes of the people holding the debt is a very different matter though!!