Do you have life insurance?

I do. I have so much life insurance, I joke that if something were to happen to me, John will be a very wealthy man.

It is a bad joke, I know. John’s been telling me that since the very first time I mentioned it.

It may be a bad joke, but it is the truth. My life is insured for close to $800,000 in two different policies; one of these is part of my pension plan.

This is quite a bit less than the amount for which David Beckham’s legs were (are?) insured but still it’s a decent amount. The way I see it, I’d rather John concentrates on looking after our son if I die in an accident, than worry about money.

And you know what? When we were in $160,000 worth of consumer debt and I was trimming our budget like you trim your roses for the winter – almost to the root – my life insurance was one item I never felt tempted to cut out.

Because, if my labour (my pay-check) was essential for the financial survival of the family I felt it is absolutely vital to ensure my family would be okay if something were to happen to me.

Similarly, we worked out the level of insurance I carry to take into account that we have a young child, that I’m the main breadwinner and that we have some liabilities.

For us, having life insurance was, and still is, as important as having a nutritious, healthy meal – it was absolutely central to our financial survival in case of unexpected and severe crisis.

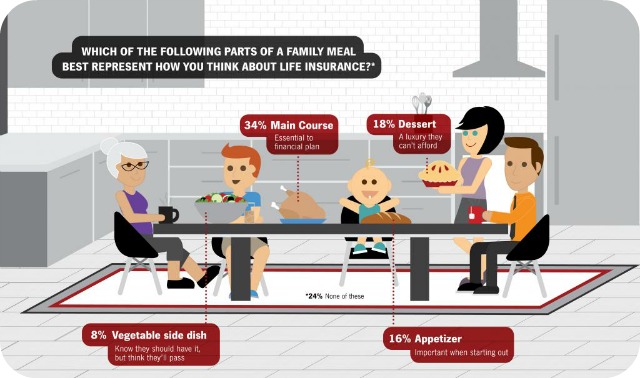

A recent survey conducted on behalf of State Farm found that 34 percent of Americans think like us and when asked to compare life insurance to parts of a family meal, said it was the “main course” in their financial plan.

Almost one in five, 18 percent, likened it to a nice-to-have dessert that they cannot afford; 16 percent thought of it as an appetizer for when you’re starting out; and 8 percent considered it a good-for-me-but-I’ll-pass vegetable side dish.

These results are interesting in their own right. What they made me think about, however, is that they are even more interesting if seen not as a snapshot of a situation but as a dynamic way to see life insurance.

After all, whether you have life insurance – and how much – depends on your personal circumstances. Hence, any decision in this respect depends on asking – and finding the answers to – the following five questions, I believe.

Q1: Do you have dependents?

Q2: Are you the main breadwinner?

Q3: How much are you worth?

Q4: What are your liabilities?

Q5: What is your pension plan?

Whether life insurance is a main meal for you, or a tempting dessert you skip on because you can’t afford it depends on your answers.

Life insurance as a main course

I believe, that life insurance is – and should be – a main meal in the context of your financial hedging if you:

- Have dependents. These can be children but equally it can be your elderly parents or you spouse. If you are likely to leave behind someone who will have a problem looking after them-selves without your income you need to carry life insurance.

- Are the main breadwinner. If you are the main breadwinner you should carry life insurance and a generous one at that. See the point about dependents above.

- Have net-worth that is low to average. This means that if something happens to you your dependents won’t be able to replace your income.

- Have liabilities. This is an important point in the decision-making process regarding life insurance and its size. When I was deciding how much insurance to carry I factored in the calculation the debt and the mortgage. After all, you really don’t want your loved ones to have to pay your debt and to find them-selves homeless.

- Have a pension plan that doesn’t include life insurance and has no provision for pension to dependents. Strange as this may sound today, I have a pension plan that will pay off a generous lump sum to John and my son in the case of my death while employed and will pay pension to my son while he is in full time education. Lucky, I know.

Life insurance as a side dish

You can see life insurance as a bit of ‘security on the side’ you can take or leave under the following conditions:

- When you have dependents but are not the main breadwinner, have considerable net-worth and low liabilities and have managed to build (are building) good retirement income (passive income)

- Another set of conditions under which life insurance can be seen as optional is if you have no dependents and are not the main breadwinner. It matters little how much is your net-worth, whether you have liabilities and what is your pension plan.

Life insurance as an appetizer

Life insurance can be an appetizer, or worth it when you are starting out, only if you have dependents (children). Otherwise, I believe, it is not very important.

Life insurance as a luxury dessert

I don’t believe that life insurance is ever a luxury dessert.

Finally…

When paying off debt it is tempting to see life insurance as a side dish that you can skip on or as a luxury dessert that you cannot afford.

This is a mistake. When coping with debt (and dealing with debt) life insurance can provide an island of stability in an otherwise turbulent financial time.

How do you view life insurance?

Disclosure: This blog post was written as part of a sponsored program for State Farm to raise awareness about the importance of life insurance. All views expressed are entirely my own, and were not influenced or directed by State Farm. You can learn more about this blogger program and life insurance at GoodNeighbors.com, PlantingMoneySeeds.com, and by following #StartLiving on Twitter.

We each have life insurance through work, but not enough. My husband definitely doesn’t have enough. We’ve discussed getting more life insurance throughout the year, but we haven’t pulled the trigger, yet. I’m sure it will happen within the next few months.

@Brandy: Go for it, Brandy; the sooner the better. Life happens to all of us and some of it is not great 🙁

I have viewed life insurance both as a main course (earlier in life) and as a side dish (currently). My goal is to be self-insured to the extent possible. We do not pay for life insurance for my wife, as her income is not essential and other funds can cover final expenses if necessary.

@Grant: Smart! My husband’d isurance is much less than mine for very similar reasons. I also thing that getting to a situation where your net-worth is high enough not to need an insurance is a great way to go.

I view it as a waste of money as I have no dependants & enough net worth to cover all my liabilities.

@Louise: Quite right; in your case it’ll be a waste of money.

We have an equal amount on each other ($800k) as we are self-employed and had a rental and three kids. Earlier this year we sold the rental and our kids are older teens, one is halfway thru a trade apprenticeship, the middle finishes high school this year and the youngest has just one left. I am thinking of reducing the amount on myself as I am not the main income of our business, we sold the rental and our kids are almost of an independent age. I’d like to leave enough cover in place so that the house and any business related debt are covered. I understand that if I want to increase the cover later it is viewed almost as a new policy and any conditions that present themselves during the interim would be excluded, so I think my husband and I need to have a chat about any 10 year plans we might have first.

@Moni: Yeah, you should be careful and check all conditions and offers in detail. One big mistale we made in the past that we were over paying for being under-insured on a policy we took out in mid-90s. When we looked around, the insurance industry is so competitive that we managed to get cheaper life insurance (higher cover) and we are older.

Life insurance isn’t on my menu…. yet. I have no dependents, spouse, nothing.

@Stefanie: Worth considering when the menu changes :).

We both have life insurance. Working in the mortuary industry taught us real quick that we never wanted to go without it. I feel confident that either one of us would be okay with the kids if something happened.