Image courtesy of ddpabumba / FreeDigitalPhotos.net

When I was a young adult there were only two options to prepare for retirement: Pensions and 401(k)s. Well, there was also Social Security – but we won’t go there!

The investing landscape has changed dramatically. The government has created other venues for tax favored accounts – and all of them are better than doing nothing.

Everyone’s situation is different. I’m not a Financial Advisor so you need to seek the advice of a trained professional but I do think Millennials have the best opportunities to become investors and get complete control over their financial destinies if they skip the 401(k) and go ROTH all the way.

Millennials jump from job to job

The employment landscape isn’t what it used to be. The average person will have 15 – 20 different jobs over the course of their working lives!

If Sally starts saving $100 a month at her new job but leaves 4 years later then she will have invested $4,800. Repeat this process for 20 years and she will have approximately $5,000 at 5 different companies (not including growth or dividend reinvestments).

Having that many different accounts gets confusing, and many young adults are tempted to cash out the plan and use the money for other things. That’s a big, costly mistake.

Maybe Sally wants to get the match? She could save 3% of her income at work to get the match (or whatever your company’s match would be) and then save more in a Roth. The benefit here is that it gives her more experience in the investing world, the best of both tax-worlds, and a place to roll her 401(k)s when she leaves (and she will leave someday).

Note: There are taxes due when converting a 401(k) to a Roth. Rolling a 401(k) into a traditional IRA would provide many of the same benefits as a Roth IRA without the tax penalty. Again, seek the advice of a trained professional when entertaining this idea.

Millennials have more options

How many funds are in your current employer’s plan? Most will have a mix of 12 – 15 (not including target-date funds). Bonds, International, large cap, small cap, blended… there isn’t a big variety to choose from.

The open market offers thousands of funds for the individual investor to choose from – with more being created every year.

If you are trying to meet, or beat, the market then picking your own mix of mutual funds and/or index funds in a Roth IRA should produce a healthier portfolio.

Do a simple search for mutual funds at Fidelity.com and you will find almost 3,000 results. Vanguard offers more than 15,000. Dude, surely you can find better funds with just a bit of research!

Millennials have time for tax-free growth

By definition a Millennial has more time to let savings grow. This plays a big part in choosing to skip the 401(k) and going with a Roth instead. A 401(k) will save you on taxes today but a Roth IRA will save you on paying taxes on the growth of your account.

By definition a Millennial has more time to let savings grow. This plays a big part in choosing to skip the 401(k) and going with a Roth instead. A 401(k) will save you on taxes today but a Roth IRA will save you on paying taxes on the growth of your account.

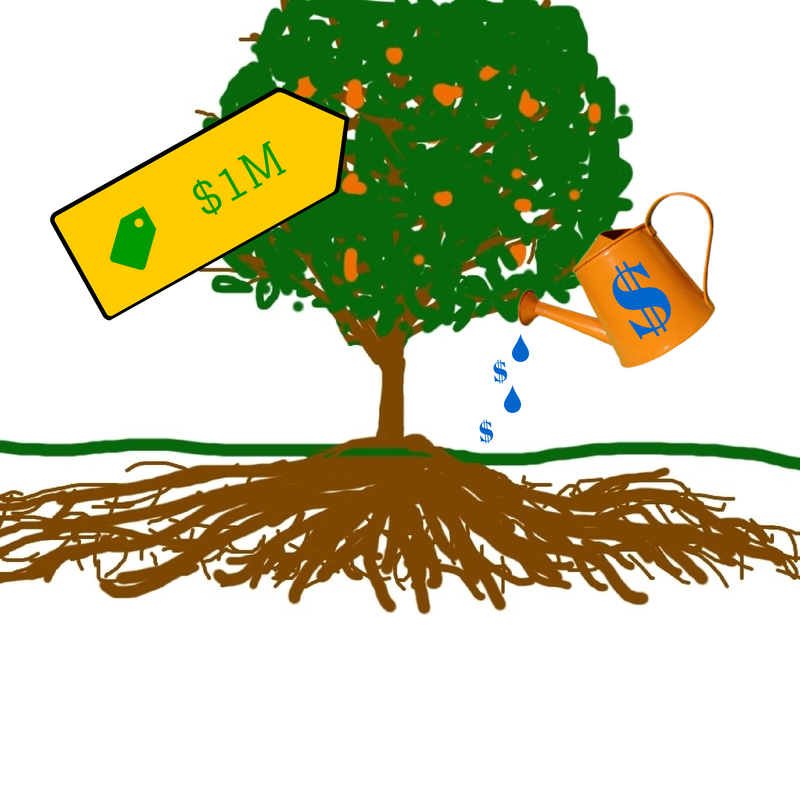

I call it the $1,000,000 tree. Let us pretend it takes $5,000 a year to grow a tree worth $1,000,000 over a 40 year period. That’s $200,000 you put into growing your tree and $800,000 is the growth.

Pre-tax savings in a 401(k) is like getting the water as a discount. Water the tree every month and you will save on the taxes. You only pay taxes when it comes to picking the fruit off the $1M tree at retirement.

There is no savings when buying the Roth water. However, you pay no taxes on the $1,000,000 tree.

So, do you want to save 15-20% on the $200,000 it took to water the tree (pre-tax) or save $800,000 in taxes because you watered the tree with after-tax dollars?

Read: Pay for the seed or the tree? Why I invest in a Roth IRA

If I knew then what I know now

There are many things to consider before deciding how to save for retirement. Time horizon, risk tolerance, fees and commissions. However, doing nothing isn’t an option.

Company-provided pensions are going away and 401(k) plans are limiting. You Millennials have got it so good!

If I could do it all over again I would skip the 401(k) and go Roth all the way.

I’m a ROTH kinda gal. I have a 401(k), but it’s through the actors union, which means it only gets funded when I have union employment- which is always sporadic. I decided I needed to take responsibility for my own retirement by making sure to fund my ROTH consistently, whether employed or not.

Stefanie, that’s crazy. It must take a lot of discipline to fund the ROTH on a sporadic income.

Do you fund your ROTH every month equally or skip a month when you can contribute to the 401k from union employment?

I’m a huge believer in both. I have a Roth and a traditional IRA. When I left my jobs that provided 401K type accounts, I did a direct transfer to the IRA. My only concern about the Roth is my lack of trust that the government won’t change the rules someday and make it taxable in some form. Oh, they won’t call it a tax. They’ll call it a service fee, or a distribution fee or something else. But the amount of money that is sitting in retirement accounts is just too tempting for the government not to drool over. Because of that, have a deductible retirement fund at least keeps it out of the hands of the gov’t. up front.

Kathy – good point. I’m also curious to see how Washington treats my Roth as I’m about to start withdrawing.

Hey, you could also look at it this way: Having both a Roth and Traditional IRA is diversifying the taxation on your retirement. Not a bad idea.

Smart post! I would’ve never thought about these long-term reasons for going ROTH only. Good info here, Steve!

Thanks Laurie. It’s not often that people consider me “smart”. I guess wisdom really is born from experience (a lot of experience).

🙂

If someone has all of their money in a Roth, they will miss out on the 0% and 10% tax brackets later. (The exception is a person with a pension or other source of taxable income). I think it is best to have both. 🙂

A person does need to consider how much they are going to contribute yearly. An IRA caps you at $5,500 if you are under age 50, so if you want to contribute more, you are going to have to take advantage of a 401k. Also, many 401k plans are offering a Roth option now, so you can take take advantage of the Roth tax advantages even though you are in a 401k.

But I do agree, if you are stuck in a 401k with high fee funds, or you want to be able to select any investments you want, an IRA is the way to go first. But it is hard to say only go IRA and forget your your 401k completely.

Agreed. Besides, there’s a really good chance a millennial will have a hodgepodge of retirement plans from all the jobs they left.

If a millennial can save $10K a year for retirement (which would be AWESOME) they could contribute half-and-half (50% ROTH 401k, 50% 401k). But they would still end up with a couple of IRAs at retirement from rolling them into their own private accounts.

There are so many options to choose from it would be impossible to make any single recommendation that works for everyone. But you are right – high fees definitely plays into this.

Steve,

If someone can’t afford to do both are you advocating ROTH over 401?

Right now I’m doing TSP (fed employee version of 401) at 5% and getting a 5% match

Assuming I can yield the same results through ROTH, I would have to put in twice as much money

OR

I’ll admit my TSP is limited in options, and while that 5% may out-perform in an aggressive / riskier ROTH the avg rate of return on my target date fund is a little over 7% since 2005 (and 14% in the last 5 years)

A ROTH with the same 5% contributions would need to hypothetically outperform my TSP with a return on 14% since 2005 (to break even) or 28% in the last 5 years…which seems unrealistic.

Have I over-simplified the math?

I’ve always considered it best to go TSP (especially if there is matching to get the free money), then go Roth.

A five percent match is pretty sweet! In your case I would definitely contribute up to the match in the TSP. It would be hard to beat that!

Then, if there was anything left over, I would save in a ROTH. Do you have access to a ROTH TSP?

Yes, I have access to the Roth TSP but not taking advantage of it right now. I could contribute to both…tradition and Roth…but when I’m ready to increase my retirement savings I was thinking outside of TSP for the reasons you stated above…more variety.

The match is pretty awesome…another company was telling me about their package and they only match 50% up to 4%

Been doing some research and didn’t realize how much packages vary from company to company

Would you be able to get the match if you contributed to the ROTH TSP? I would totally do that instead of the traditional side of the TSP. That way you save tons of money that will grow tax-free and the match goes into a tax-deferred account. You don’t get any tax savings today, but the match is free money anyway.

When it comes to tax savings in retirement plans it’s pay-me-now or pay-me-later. The only question is do you want to pay a little in taxes today or a lot on the huge portfolio you built?

If you go outside of your work then be aware of contribution limits. That is all.

For my first two years since graduating college I have maxed out my Roth IRA both years while contributing to my 401k at 6% to get the 3% match. When I received a raise I bumped that 6% to 8%, but 3% is still the maximum match that I get from my company. They also offer a pension that is just straight 3% of your salary (so another free 3% “raise”) each year which gets around 1% interest as well.

I think when I’m done paying off my debt I will increase my 401k though, as it is still a tax advantage account and I’m lucky to have relatively low fees. I believe the fees are only 0.02% higher than the Vanguard target date funds I used for my Roth IRA so the match more than makes up for that.

Dude, you are ROCKIN it!

How much debt have you got? If you cut back on your 401k, just to the match, could you knock it out in a year?

Currently, I invest in both a 401k and a Roth. I only contribute enough in my 401k for the match, though. The rest goes toward maxing out my Roth IRA! I’ve had to roll over my previous 401k into a Traditional IRA, but the process isn’t too bad!

See! You are doing it – the best of both worlds. I’m assuming you have done this recently? I’d love to hear about your experience.

The author of this article obviously doesn’t understand basic math. If you are in the same tax bracket when you are working as you are when you retire, there is no difference in the growth or taxes paid on a 401K or a ROTH account.

I don’t understand your comment JD. As I understand it, there is a huge difference in taxes paid on a 401k as we take it out of retirement than a ROTH would.

If I funnel $100,000 into a retirement account that grew to $500,000 then there would be a huge difference: I would have paid taxes on $100,000 of income when saving into a ROTH but not have to pay taxes on the growth whereas I get a tax break today for a 401k but have to pay taxes on $400,000 of growth.

Can you reply again and show me where I am wrong?

Hi Steve,

It is incorrect to compare 100k of Roth contributions with 100k of traditional 401k contributions as though they are equivalent. They are not. You acknowledge this difference with your words but not with your calculations.

Compare a portfolio of 133,333 in tax deferred and 100k in a Roth (assuming 25% tax rate). The 133k portfolio will cost 100k, the same as the Roth portfolio. Compound them both over some period of time, reduce the tax deferred by 25%, and compare the results. You will see that they are equal.

This will always be true as it is the very definition of the commutative property of multiplication, a law of mathematics.

Regards,

Petunia 100

I see what you are saying – that it takes more than $1 to put a dollar into a ROTH because of taxes. However, isn’t it true that much of the overall impact to our finances would be dependent on the ROR, your tax rate at retirement, and overall tax strategy?

Here’s what I mean: We can’t forecast what the market will do over the next few decades, can’t predict what our tax rate will be at retirement, and can’t predict other assets we might own that change our entire income strategy (ie: Real estate or passive income from a business vs investment income). If I’m building wealth over a long period of time and have quite a bit of taxable income at retirement then taking a ROTH out of the equation would be beneficial to my overall withdrawal strategy.

Oh no, we’re dipping our toes into financial planning now. I’ll have to stop and let you have the next word. 🙂

Absolutely, there are a lot of unknowns. And of course, our financial situations vary so much from person to person.

I have both tax-deferred and Roth, because I think that is the best approach for me. 🙂